Navigation

TRIAL BALANCE

1. Introduction and Meaning

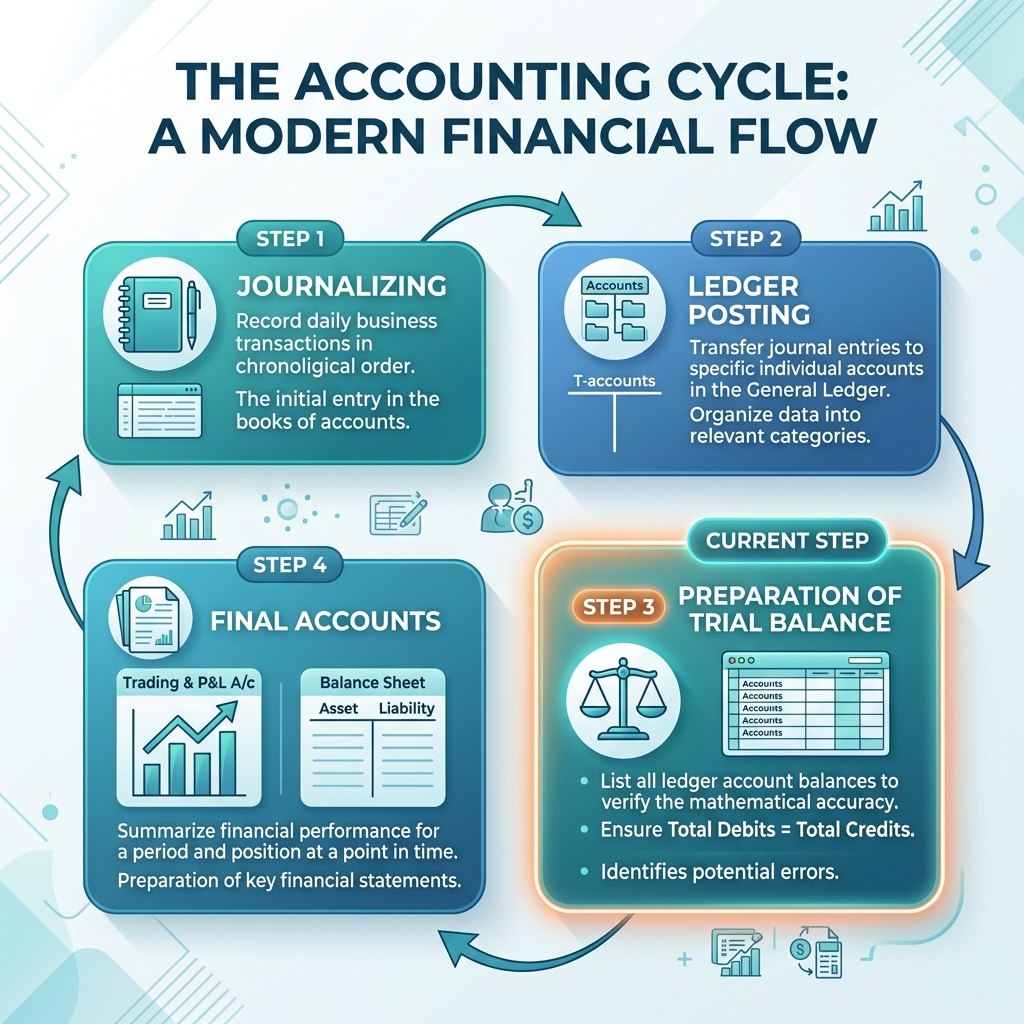

After recording transactions in the journal and posting them to the ledger, the next step in the accounting cycle is to prepare a Trial Balance. It is a statement that lists all the ledger account balances (debit and credit) on a specific date. Its primary purpose is to verify the arithmetical accuracy of the books of accounts – i.e., to check whether total debits equal total credits.

The Trial Balance is not a part of the final accounts; it is an intermediate statement that helps in preparing the Trading and Profit & Loss Account and the Balance Sheet.

[!NOTE]

Definition (J.R. Batliboi): “Trial Balance is a statement, prepared with the debit and credit balances of the ledger accounts, to test the arithmetical accuracy of the books.”

2. Definitions from Experts

| Expert | Definition |

|---|---|

| Spicer & Pegler | “A trial balance is a list of all the balances standing on the ledger accounts and the cash book.” |

| Roland | “The final list of balances, totaling the debit and credit columns of the ledger that are finally equal is known as Trial Balance.” |

| M.S. Gosav | “A trial balance is a statement containing the balances of all ledger accounts as on any given date.” |

3. Objectives of Preparing Trial Balance

The main reasons for preparing a Trial Balance are:

- To Check Arithmetical Accuracy: If the total of the debit side equals the credit side, it proves that the books are arithmetically correct.

- To Help Prepare Final Accounts: It provides a summary of all balances in one place, making it easier to prepare the Trading A/c, P&L A/c, and Balance Sheet.

- Summary of Each Account: It serves as a condensed version of the entire ledger.

- To Locate Accounting Errors: If the Trial Balance doesn't agree, it alerts the accountant that an error occurs in journalizing or posting.

4. Features of Trial Balance

- It is a statement, not an account.

- It is prepared on a particular date (usually at the end of the year).

- It contains both debit and credit balances of ledger accounts.

- The total of the debit column must always equal the total of the credit column (Double Entry System).

- Agreement of Trial Balance is not conclusive proof of absolute accuracy (certain errors like Principle errors may still exist).

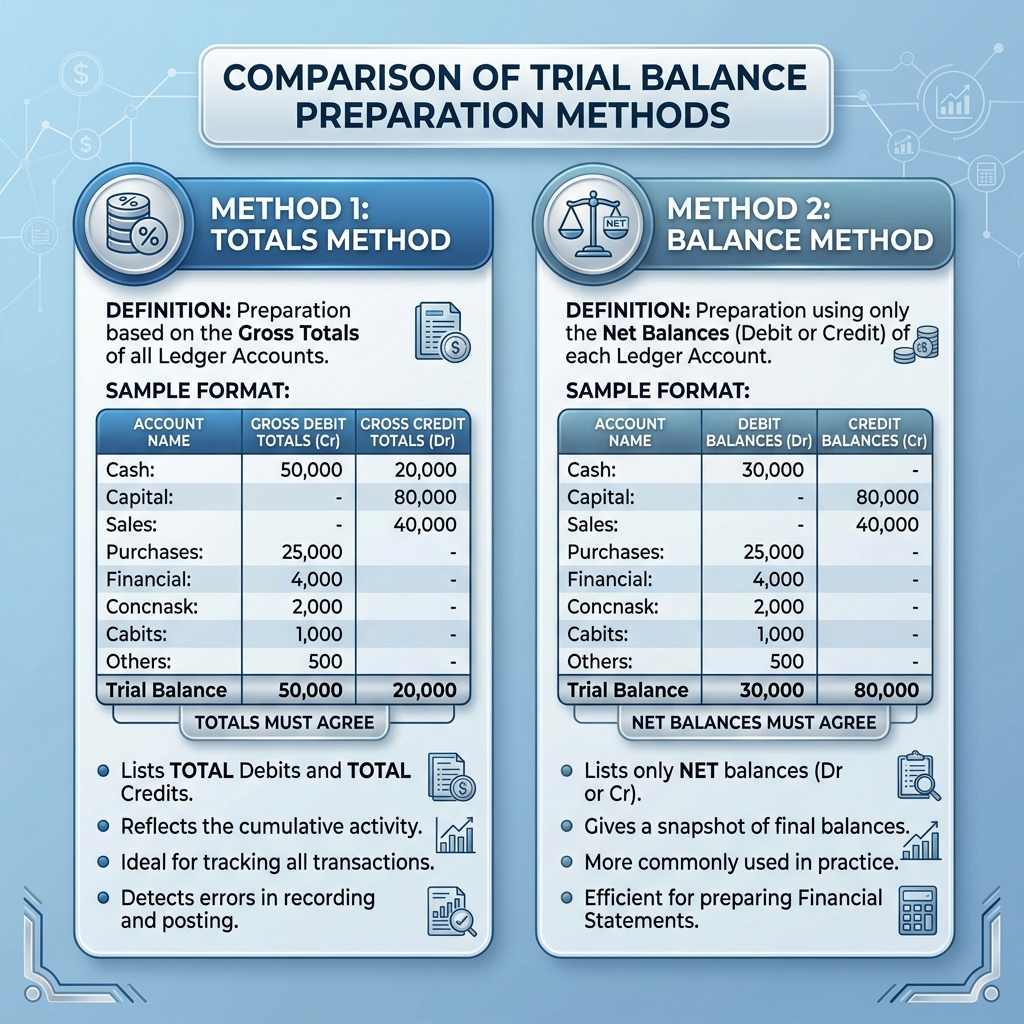

5. Methods of Preparing Trial Balance

There are three main methods:

- Totals Method (Gross Trial Balance): The total of the debit side and credit side of each ledger account is shown in the Trial Balance.

- Balance Method (Net Trial Balance): Only the net balance (debit or credit) of each ledger account is shown. This is the most common method.

- Totals-cum-Balance Method: A combination of both methods, using four columns for each account.

6. Steps to Prepare Trial Balance (Balance Method)

- Balance all ledger accounts: Find the difference between the debit and credit sides of each account.

- List Account Titles: Write the names of all accounts in the first column.

- Enter Debit Balances: Accounts showing a debit balance (Assets, Expenses, Drawings) are entered in the Debit column.

- Enter Credit Balances: Accounts showing a credit balance (Liabilities, Incomes, Capital) are entered in the Credit column.

- Total Both Columns: Calculate the sum of both columns and ensure they match.

7. Format of Trial Balance

Trial Balance of M/s [Business Name] as on [Date]

| S.N. | Name of Account | L.F. | Debit Balance (₹) | Credit Balance (₹) |

|---|---|---|---|---|

| 1 | Cash Account | xxx | ||

| 2 | Bank Account | xxx | ||

| 3 | Purchases Account | xxx | ||

| 4 | Sales Account | xxx | ||

| 5 | Capital Account | xxx | ||

| 6 | Sundry Creditors | xxx | ||

| 7 | Salaries Account | xxx | ||

| 8 | Furniture Account | xxx | ||

| Total | XXX | XXX |

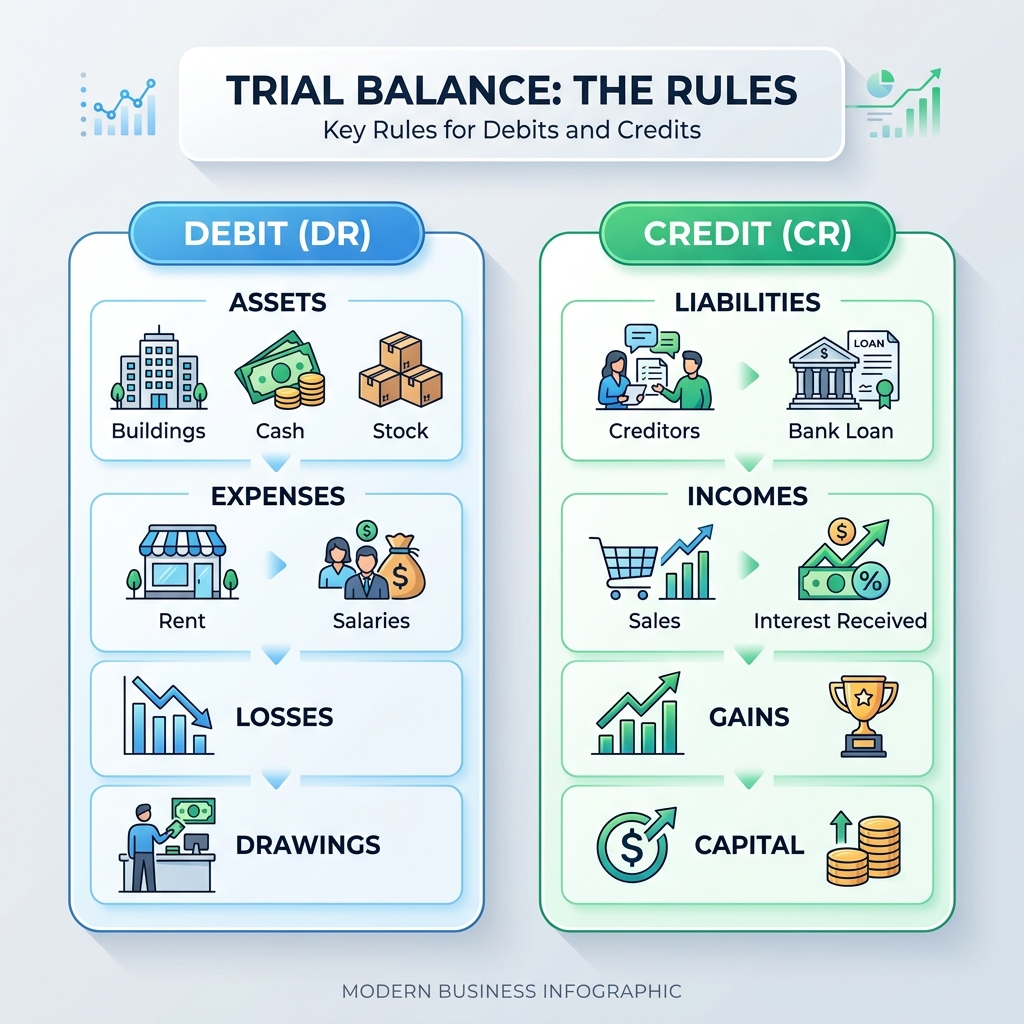

8. Rules for Placing Accounts in Trial Balance

To avoid confusion, use this simple logic:

- DEBIT SIDE (Dr.):

- Assets (Cash, Bank, Building, Machinery, Debtors)

- Expenses & Losses (Purchases, Rent, Salary, Depreciation, Bad Debts)

- Drawings

- Sales Return (Return Inward)

- CREDIT SIDE (Cr.):

- Liabilities (Creditors, Bank Loan, Bills Payable)

- Incomes & Gains (Sales, Interest Received, Commission Received)

- Capital

- Purchases Return (Return Outward)

9. Difference: Trial Balance vs. Balance Sheet

| Feature | Trial Balance | Balance Sheet |

|---|---|---|

| Nature | A statement to check accuracy. | A statement of financial position. |

| Object | To check ledger balances. | To show assets and liabilities. |

| Content | Includes Real, Personal, and Nominal accounts. | Includes only Real and Personal accounts. |

| Closing Stock | Generally not included. | Must be included. |

| Status | It is not part of Final Accounts. | It is the final statement of an enterprise. |

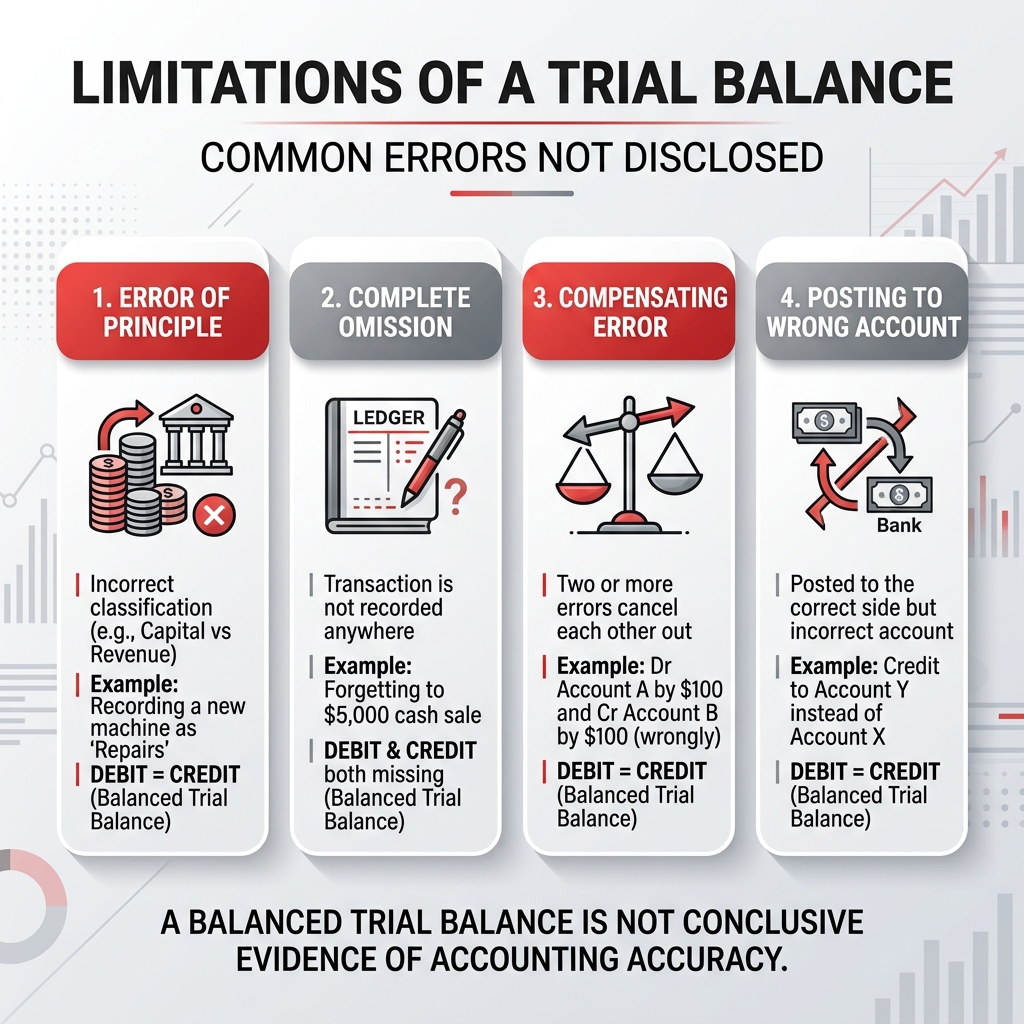

10. Errors Not Disclosed by Trial Balance

Even if the Trial Balance agrees, these errors might still exist:

- Error of Omission: A transaction is completely missing from the journal.

- Error of Principle: Capital expenditure recorded as revenue expenditure (e.g., Repair to machinery debited to Machinery A/c).

- Compensating Errors: Two or more errors cancel each other out.

- Error of Commission: Writing the correct amount on the wrong side or wrong account but on the same side.

- Posting to Wrong Account: Entry posted into the wrong personal account (e.g., Debited A instead of B).

11. Practice Examples

Problem 1: Prepare a Trial Balance

From the following balances of Mr. Verma as on March 31, 2025:

- Cash in Hand: ₹5,000

- Bank Balance: ₹12,000

- Purchases: ₹1,50,000

- Sales: ₹2,20,000

- Capital: ₹1,00,000

- Rent Paid: ₹10,000

- Salaries: ₹20,000

- Sundry Debtors: ₹40,000

- Sundry Creditors: ₹30,000

- Machinery: ₹80,000

- Drawings: ₹5,000

- Returns Inward: ₹2,000

- Returns Outward: ₹1,000

- Interest Received: ₹3,000

12. Conclusion

The Trial Balance is a vital tool for ensuring the integrity of the accounting system. While it guarantees arithmetical accuracy, accountants must remain vigilant for conceptual errors that do not affect the balance but distort the financial truth.

Practice MCQs

[!TIP]

Master the concepts of Trial Balance and Error detection with 30 custom MCQs designed for academic and competitive success.